In today’s deeply connected world, the size of a country’s economy affects almost every part of daily life, even for people who never think about economics. The food we eat, the phones we use, the jobs that are created, and even the prices we pay are influenced by how strong or weak major economies are. When the world’s largest economies grow, global trade usually expands, investment increases, and new opportunities are created. When they slow down, the effects are often felt far beyond national borders.

The term “largest economy” is most commonly measured using Gross Domestic Product (GDP). GDP shows the total value of all goods and services produced within a country during one year. It is not a perfect measure of happiness or quality of life, but it is the most widely used tool for comparing economic size across countries. This article is based on nominal GDP, which measures output using current US dollar values, the same method used by global institutions and explained by Investopedia.

1. United States

The United States has remained the largest economy in the world for decades, and its position continues to be maintained because of its diverse and highly productive economic structure. With a GDP of around $30 trillion, the U.S. economy produces more goods and services than any other country. This size is not created by one single industry, but by a powerful combination of services, technology, manufacturing, finance, healthcare, and consumer spending.

Most of the U.S. economy is driven by services rather than factories. Banking, insurance, education, entertainment, healthcare, and professional services contribute heavily to national income. At the same time, the country is home to many of the world’s most valuable companies, especially in technology and innovation. These companies sell products and services globally, which allows money to flow into the American economy from nearly every region of the world.

GDP growth in the United States has been relatively stable over time, with slower growth during global crises and stronger growth during recovery periods. Even when growth slows, the sheer size of the economy helps protect it from sudden collapse. Because the U.S. dollar is also the world’s main reserve currency, the country holds a unique and powerful position in global finance.

2. China

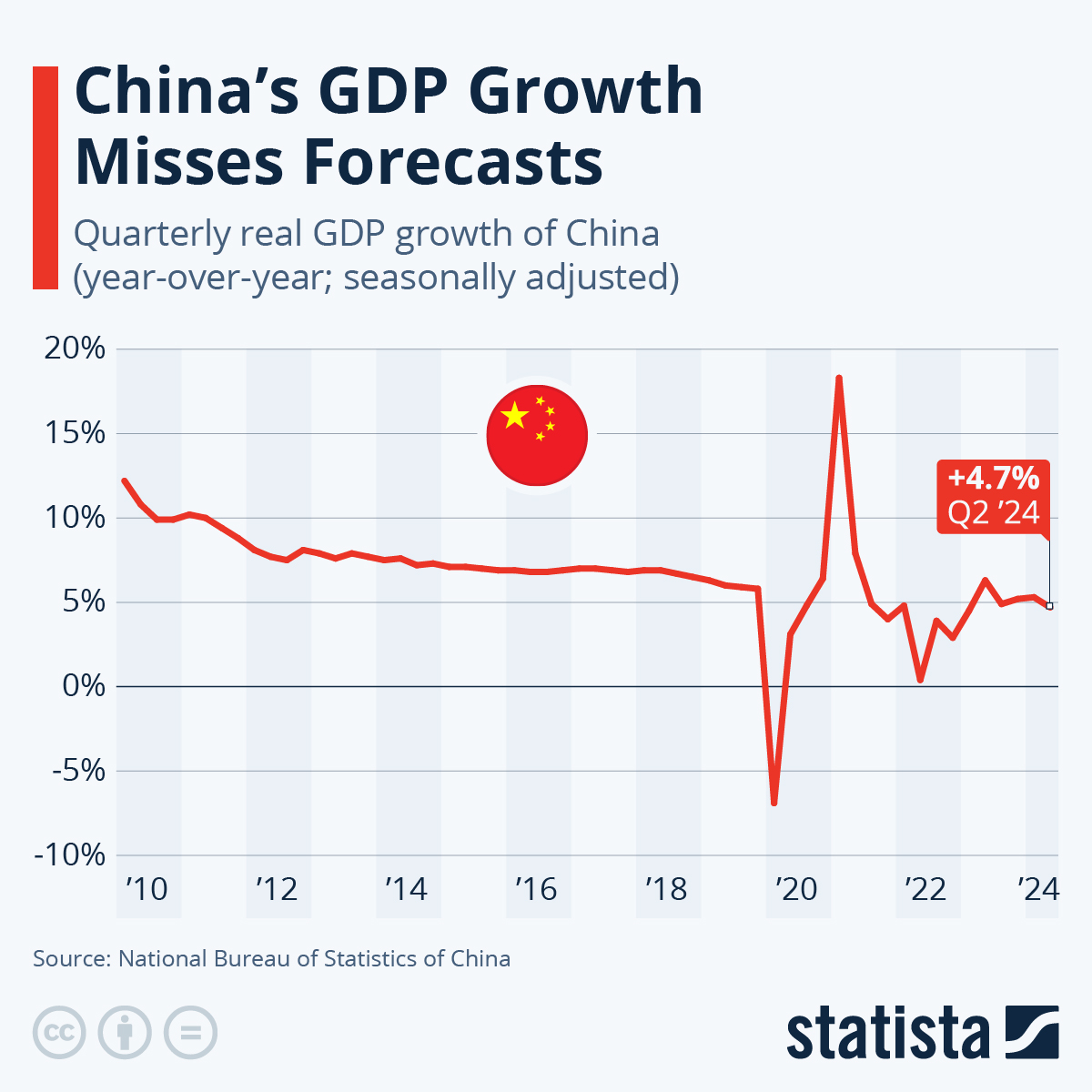

China is the second-largest economy in the world and has experienced one of the fastest economic transformations in human history. Only a few decades ago, China was largely rural and agricultural. Today, it is a global manufacturing center and a key driver of international trade. With a GDP of nearly $19 trillion, China’s economy is shaped by factories, exports, infrastructure investment, and an increasingly important technology sector.

For many years, China’s GDP growth rate was extremely high, often reaching levels far above those of developed economies. This rapid growth was driven by low-cost manufacturing, strong government investment, and expanding exports to the rest of the world. Over time, China has also invested heavily in transportation networks, cities, and industrial zones, all of which supported economic expansion.

In recent years, growth has slowed somewhat as the economy has matured. Domestic consumption and services are now being encouraged to replace export-only growth. Even with slower growth rates, China’s economy continues to expand because of its massive population and industrial capacity. Its GDP growth chart clearly shows a long upward trend, reflecting decades of economic expansion.

3. Germany

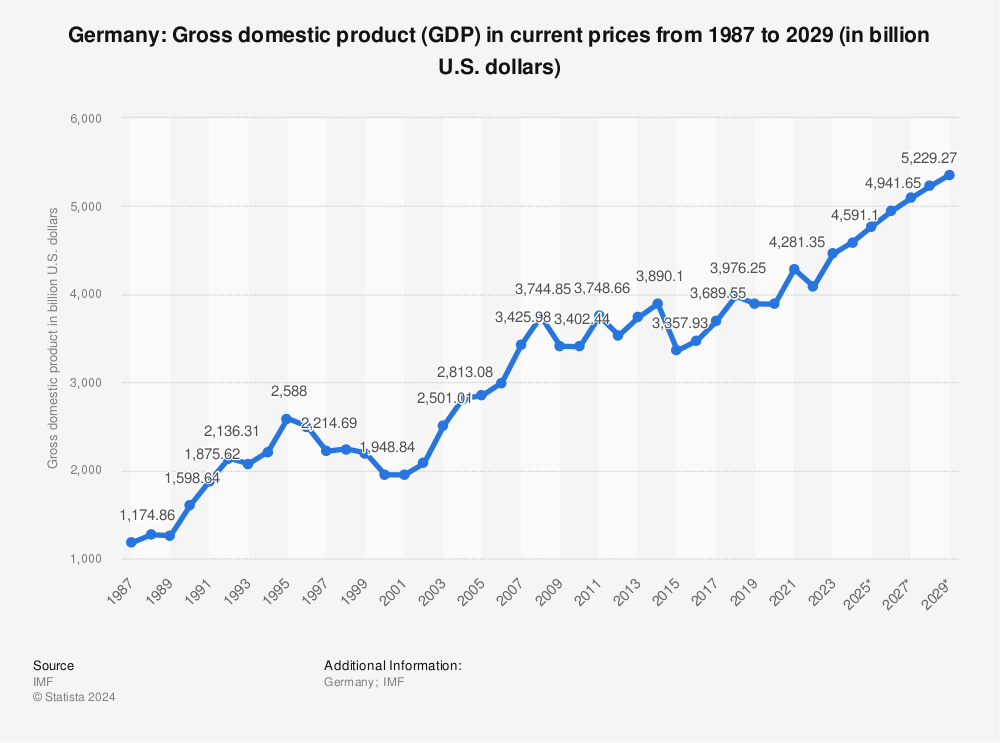

Germany is the largest economy in Europe and one of the strongest manufacturing nations in the world. With a GDP of around $5 trillion, Germany’s economic success is built on precision engineering, advanced manufacturing, and exports. German products, especially automobiles, industrial machines, and chemical goods, are known globally for their quality and reliability.

Unlike many large economies that depend heavily on consumer spending, Germany relies strongly on exports. A large share of what is produced in Germany is sold abroad, which allows the country to earn income from global markets. This export-focused model has made Germany especially important to the European Union, where it often acts as an economic leader.

GDP growth in Germany tends to be steady rather than explosive. Growth slows during global downturns because of reduced trade, but recovery usually follows as global demand returns. The GDP growth chart shows moderate rises over time, reflecting stability rather than rapid expansion.

4. Japan

Japan is one of the most advanced economies in the world and ranks among the top four globally. With a GDP of about $4.3 trillion, Japan’s economy is highly developed, technologically advanced, and deeply integrated into global trade. Major industries include automobiles, electronics, robotics, and precision equipment.

Japan’s economy grew extremely fast in the decades after World War II, turning the country into a global industrial leader. However, in recent years, economic growth has been slower. An aging population and low birth rates have reduced the size of the workforce, which affects long-term expansion.

The GDP growth chart for Japan shows periods of strong growth in the past and flatter growth in recent years. Even so, Japan remains economically powerful due to its innovation, skilled workforce, and strong global brands.

5. India

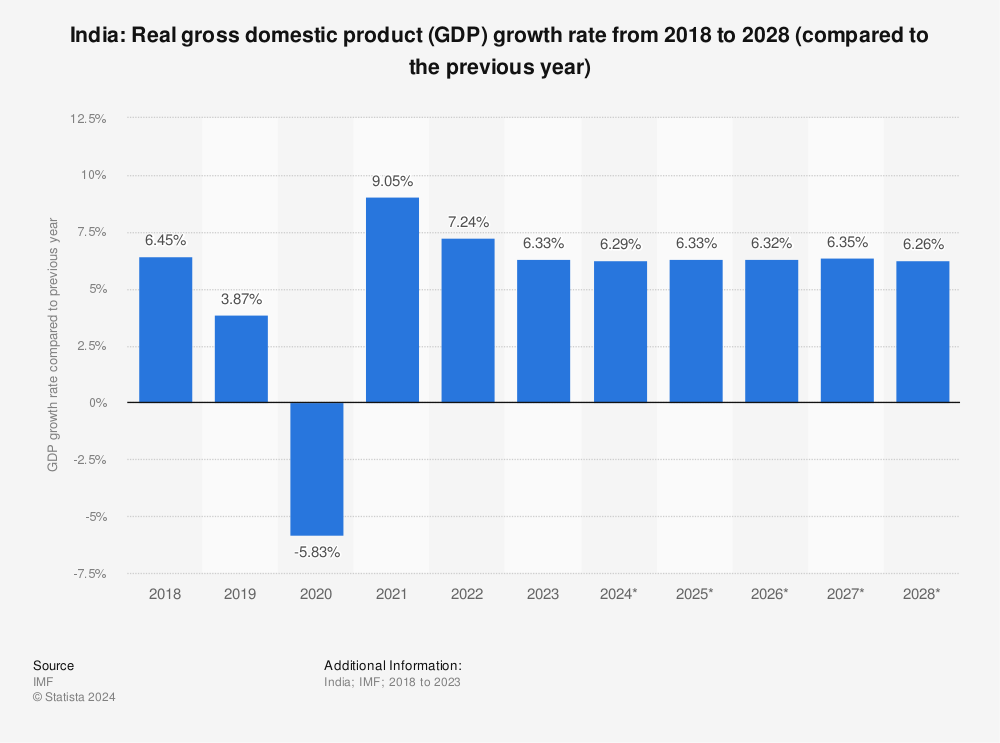

India is currently the fifth-largest economy in the world and one of the fastest-growing among major nations. With a GDP of over $4 trillion, India’s economy is being shaped by population growth, expanding technology services, manufacturing, and domestic consumption.

A major strength of India’s economy is its young and growing population. Millions of people are entering the workforce every year, which supports production and consumption. The country has also become a global center for software development, IT services, and digital innovation.

India’s GDP growth chart shows a strong upward trend, with brief slowdowns during global crises. Because of its growth speed, India is often expected to move higher in global rankings in the coming decades.

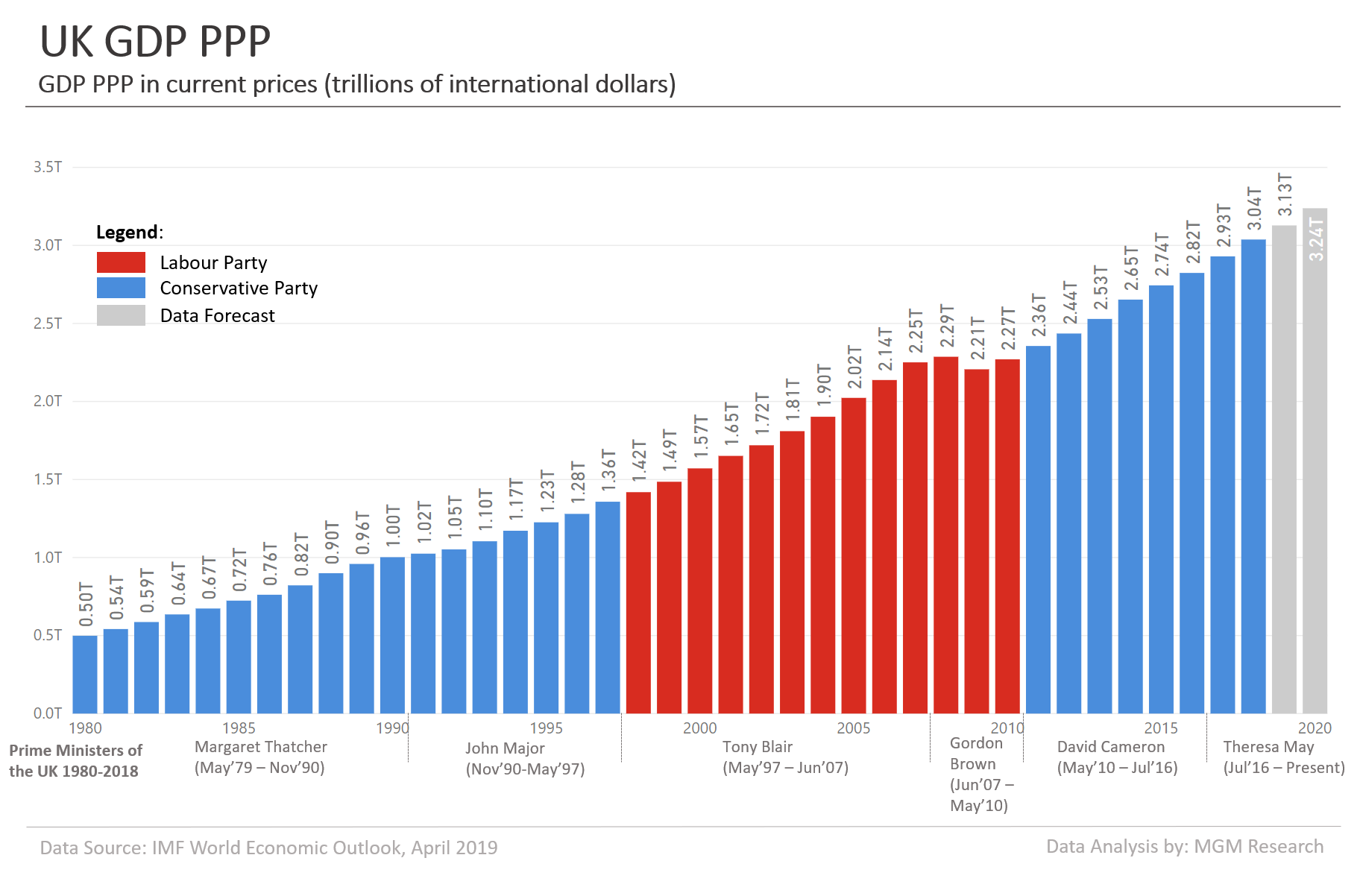

6. United Kingdom

The United Kingdom has one of the world’s most service-focused economies, with a GDP of nearly $4 trillion. Finance, banking, insurance, education, and professional services form the backbone of economic activity. London, in particular, plays a central role as a global financial hub.

Although manufacturing exists, the UK economy depends more on services than factories. This structure has allowed the economy to remain large even after major political and trade changes, including Brexit. GDP growth has fluctuated, but long-term stability has been maintained.

The GDP growth chart reflects both resilience and adaptation, showing how the economy has adjusted to global and regional changes.

7. Franc

France holds the seventh position among the world’s largest economies, with a GDP of about $3.4 trillion. The French economy is balanced across manufacturing, services, agriculture, and tourism. It is also known for strong government involvement in social services and public infrastructure.

Tourism plays a major role, with millions of visitors contributing to national income every year. Luxury goods, food exports, and aerospace manufacturing also strengthen the economy. GDP growth in France tends to be moderate, reflecting stability rather than rapid expansion.

The growth chart shows steady progress over time, with temporary slowdowns during global crises.

8. Italy

Italy’s economy, with a GDP of about $2.5 trillion, is shaped by history, culture, and industry. Manufacturing, especially in machinery, vehicles, and fashion, remains important. Tourism and food exports also contribute significantly.

Economic growth has been slower compared to other large economies due to high public debt and structural challenges. Still, Italy remains a major global producer and exporter. The GDP growth chart shows slower growth, but long-term economic importance remains clear.

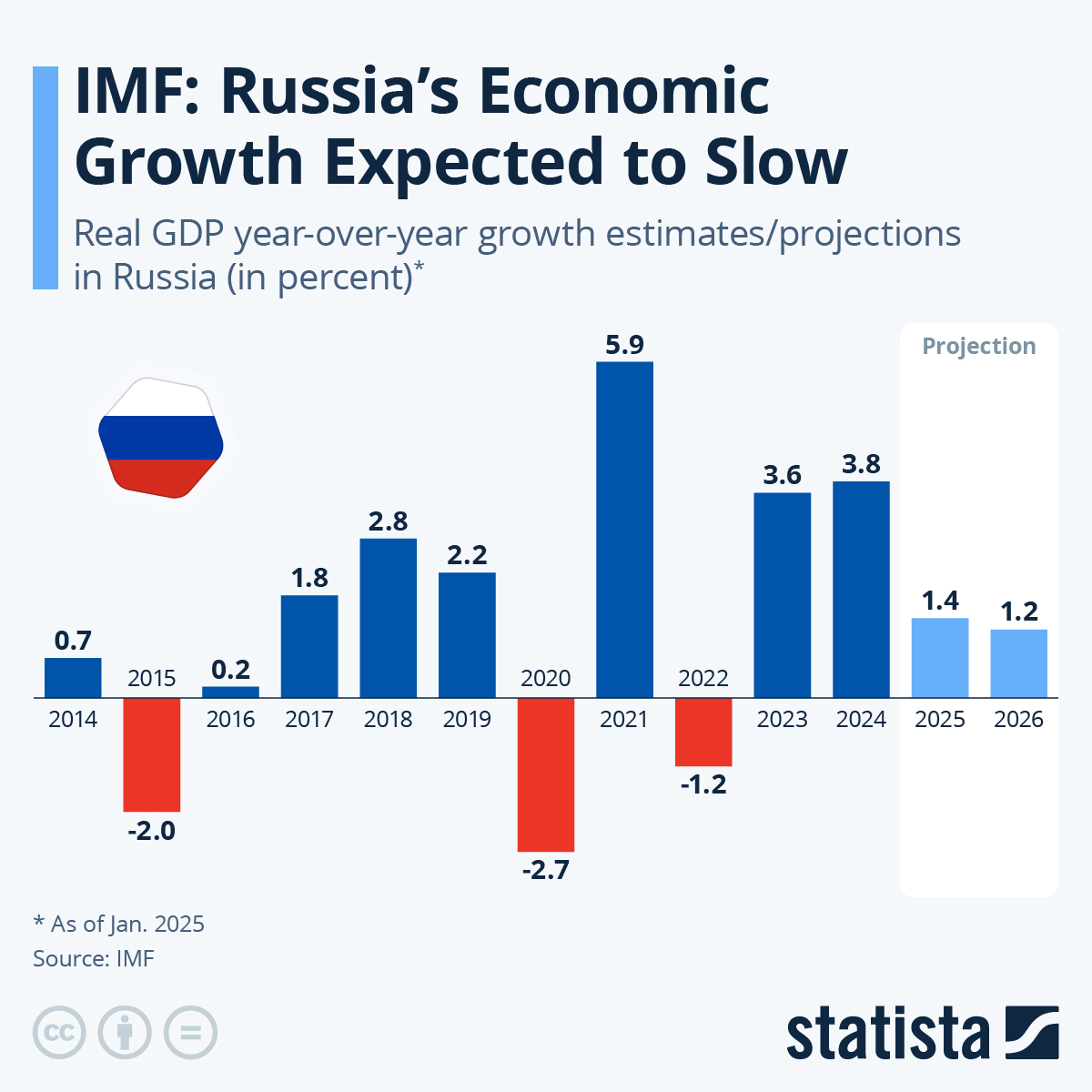

9. Russia

Russia’s economy is heavily influenced by natural resources, especially oil and natural gas. With a GDP of about $2.5 trillion, Russia plays a major role in global energy markets.

GDP growth in Russia often rises and falls with global energy prices. The growth chart reflects these fluctuations clearly. Despite volatility, Russia remains one of the world’s largest economies due to its resource wealth.

10. Canada

Canada completes the top ten with a GDP of around $2.3 trillion. Its economy is supported by natural resources, manufacturing, services, and strong trade ties with the United States.

Canada’s GDP growth chart shows steady, stable growth over time. Political stability, strong institutions, and access to resources help maintain its position among the world’s largest economies.

Why These Economies Shape the World

The ten largest economies in the world represent the core of global production, trade, and innovation. While each country follows a different economic path, all share the ability to influence markets far beyond their borders. By understanding how these economies grow and change, a clearer picture of global power and future opportunities is formed.