Former U.S. Treasury Secretary and Goldman Sachs co-chairman Robert Rubin has delivered a stark warning to financial markets: remember October 19, 1987. Speaking at the CNBC CFO Council Summit in Washington, D.C., Rubin said that the factors contributing to today’s economic complacency bear troubling similarities to the conditions leading up to the infamous Black Monday crash.

Rubin emphasised that while current discussions often revolve around tech valuations and the potential of an emerging AI bubble, the deeper risk lies in the United States’ accelerating national debt and the political system’s unwillingness to address it. He argued that ignoring these structural risks is reminiscent of the years before the October 1987 collapse, when markets continued to rise despite glaring excesses—until, suddenly, they did not.

Debt Risks That Markets Are Choosing Not to See

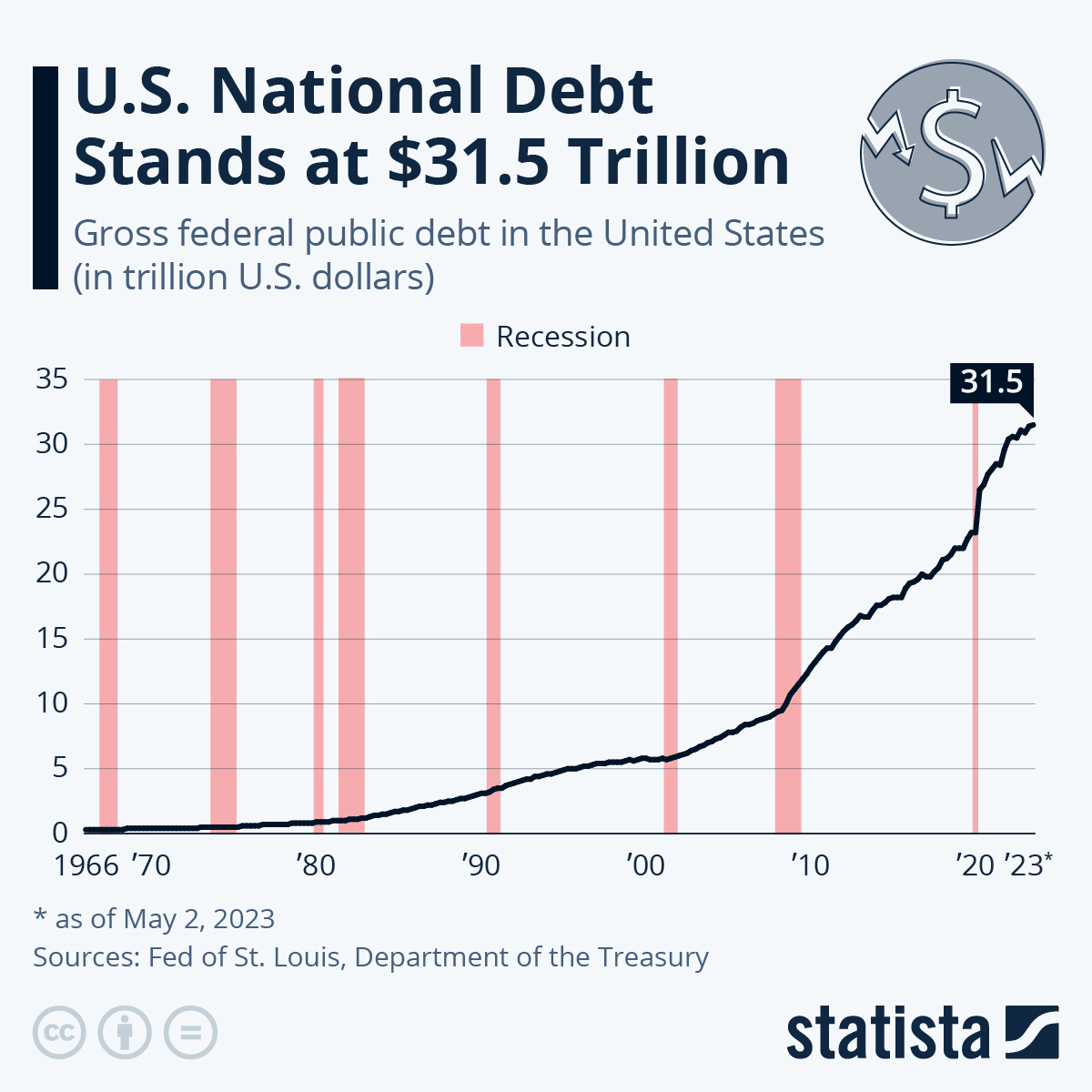

Rubin has long raised alarms about unsustainable fiscal conditions, and at Wednesday’s summit he pointed to new data from the Congressional Budget Office. Publicly held U.S. federal debt is projected to be 99.8% of GDP in fiscal year 2025, nearly double the 50-year average of 51%. But Rubin said the trend is even more worrying when viewed historically: in 2000, the ratio was just 30%. The CBO expects another 20-percentage-point rise within a decade, yet Rubin believes this projection is “optimistic.”

He cited research from Yale’s Budget Lab projecting a far steeper trajectory, with the debt-to-GDP ratio potentially reaching 130% to 140%, excluding the effects of tariffs. Some consequences are already visible, Rubin said, including reduced spending on public investment and national security, as well as upward pressure on interest rates. Business confidence may also be eroding at the margins.

But Rubin’s core message was that the real danger is ahead: the “ultimate serious consequences” that he considers highly likely, even if the timing is impossible to predict.

Why Rubin Keeps Returning to 19 October 1987

Rubin told CNBC’s Leslie Picker that when he speaks with market participants, he urges them to remember the conditions leading up to Black Monday, when the Dow Jones Industrial Average collapsed more than 22% in a single trading day. For years prior to the crash, he said, markets were “highly in excess and nothing happened.” This created a sense of indifference—investors stopped listening, convinced that risk no longer mattered.

On October 19, 1987, the illusion ended. Rubin underscored that no single event triggered the crash; it was simply markets becoming “out of sync with reality.” He fears a similar reckoning could emerge from today’s fiscal imbalances. Even if the debt dynamic has not yet produced severe consequences, he warned, markets may be vastly underestimating how quickly conditions can shift.

AI, Market Froth, and a System Unprepared for Disruption

Although much of the current attention is on whether artificial intelligence has produced unsustainable valuations, Rubin said the AI debate—while valid—is not the primary systemic risk. Short seller Michael Burry recently warned that an AI-driven bubble could unwind within two years, but Rubin sees AI’s significance extending far beyond short-term valuation swings.

For companies without established revenue engines, like OpenAI, the massive capital investments in data centres and infrastructure carry meaningful financial risks.

He also stressed that potential labour displacement is not a hypothetical issue. Some estimates suggest AI could affect up to 50% of white-collar jobs over time. Rubin noted that the exact figure matters less than the underlying trend: the U.S. political system is not preparing for large-scale transformations in employment, nor is it grappling with the fiscal implications of such disruption.

A Political System Unwilling to Face Reality

Rubin said that during his time leading Goldman Sachs he stressed to colleagues the importance of staying “actively involved and fully engaged.” Today, he sees the opposite: a political environment where lawmakers avoid dealing with rising debt, geopolitical risk, and profound technological change. These intersecting pressures, he said, create many possible paths “for things to go wrong.”

His analysis with Yale’s Budget Lab suggests that stabilising the debt-to-GDP ratio at its current level—near 100%—would require shifting the deficit by roughly 2.5 percentage points. A reasonable mix, he said, would be:

-

0.5 percentage points from spending cuts, and

-

2 percentage points from additional tax revenue.

Such adjustments would place the U.S. in a “far better place going forward.”

Growing the economy fast enough to erase debt concerns is unrealistic, Rubin added. The growth rates required would be “astronomically greater than anything that is realistic.”

Rubin’s Closing Warning: Complacency Itself Is the Risk

Rubin acknowledged the possibility that the system may continue, unsustainably, without immediate consequence: “Maybe it will never happen. Maybe we just keep going along.” But he believes that taking such a bet is profoundly unwise.

Ultimately, Rubin’s message to the market is simple: risks compound quietly—until they don’t.

And when the reckoning arrives, he says, “it will all matter… when it does.”